Liberals v Bankers as The Greek Depression ignites

But there is a third choice—a rational choice—if undertaken, will serve as the blueprint to future sovereign debt crises, of which there will be plenty.

The two forces in play in the Greek debt crisis occupying the most media coverage are the American liberals and the crony-bankers. This Hobson’s choice plays out as even more money printing, advocated by the liberals, versus austerity and reforms, advocated ostensibly by the economic rationalists. But there is a third choice—a rational choice, a just way, a fair resolution—a choice, if undertaken, will serve as the blueprint to future sovereign debt crises, of which there will be plenty.

This is how simple it is—Imagine—an unkempt, homeless man, obviously drunk, walks into a bank and asks for a loan. The bank officer does not throw him out and does some research, only to find out that the man is unemployed, has no assets, and only wants the money for more alcohol. He makes the loan anyway. Now the drunk can’t repay so the bank chiefs ask the local council ratepayers to restore the bank’s losses.

The liberals want the bank to make another loan, the proceeds of which will “repay” the first loan, so that they can pretend that all is fine. They then want the second, the drunk-loan, to be converted into securities that they want to buy with counterfeit money that they treat as real money in the hope that the drunk will eventually get sober and get a job, as the buying of securities will somehow stimulate the drunk to become sober; they believe it does. Meanwhile, the cronies want to deprive the drunk’s family of food and water, so if they risk dying of starvation and dehydration, it will shock the alcoholic into working hard. Both sides want the bank to be repaid in full.

When a sovereign state creates mountains of unrepayable debt, there is an inflection point when the fantasy ends and reality sets in.

What is the correct solution here? Well, we would sack the bank officer, require the bank to take the hit, hope that the alcoholic becomes sober, gets a job, and, in the future, spends less than he earns. We could try to inspire him, watch his progress, hope for the best, and even lend him money eventually if he proves his redemption—but that’s going to take years of good behaviour.

When a sovereign state creates mountains of unrepayable debt, there is an inflection point when the fantasy ends and reality sets in. At this point, there are three ways out:

- Austerity

If the state wishes to continue borrowing from the same lenders, it must spend a lot less than it receives, and give the surplus to the lenders. This imposes severe hardship on its citizens, only some of whom benefited from the handouts of the old drunkard-loans. It craters the economy, making tax revenue harder to obtain.

- Theft

If the state can print money, it prints enough money to repay the debt it issued. But this is no magic pill. This devaluation of purchasing power effectively steals money from retirees, savers, the unemployed, and the poor. People can be so deprived of necessities that they may die in the streets. Endemic violence can erupt.

- Repudiation

A default happens when any part of due interest or principal is not repaid on its due date, often due to inability to pay. Repudiation is different. Repudiation is an outright refusal—the unwillingness, not inability, to pay interest or principal that is due. If the lender has security over your assets, even default, let alone repudiation, gives the lender the right to repossess your assets. Otherwise, the lender can seek redress in a court of law. But a sovereign always has the right of repudiation, including absolute repudiation—the absolute refusal to pay any interest or principal that is due a lender. The lender pays for her absolute stupidity, and the sovereign borrower walks away.

More than at any other time in history, today when the bulk of even the developed world has mountains of unrepayable debt, absolute repudiation is by far the best course of action. In one instant, the sovereign can no longer borrow money and is immediately forced to “balance its own budget,” to spend no more than it earns. It’s true that some lenders may become insolvent. That will inflict pain, but there is no painless solution possible.

Why is it, that pain is unavoidable?

Let’s imagine that a ship worth hundreds of millions of dollars sinks. The salvage operation would cost more than the worth of the ship, and the ship, even if salvaged, is unlikely to work. The value is lost. Let’s say the corporation that owned it had insurance and the insurer had a reinsurance-style default swap with a bank. The fine-print-in-the-contract game that then plays out between the corporation, the insurer, and the bank, is about “who takes the hit,” for everyone knows—someone has to take it.

Who should bear the Greek hit?

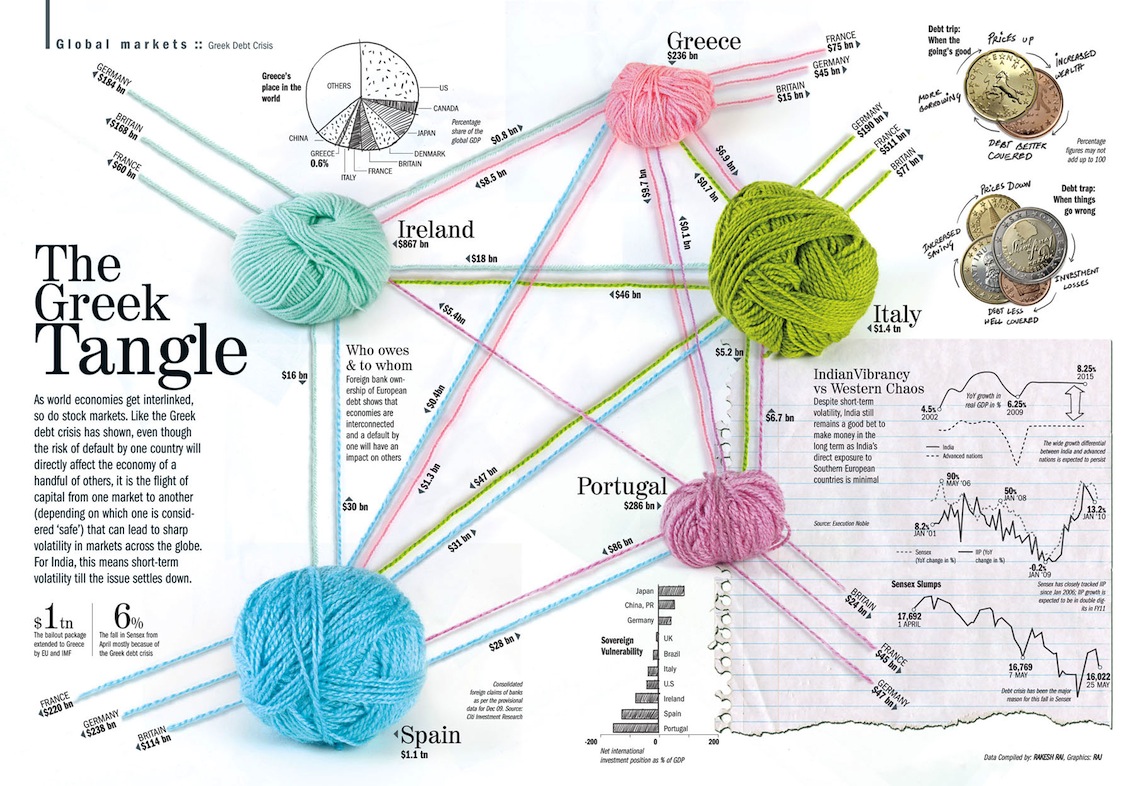

At the beginning of 2015, Greek government debt stood at 323 billion euros ($366 billion), over 175% of the country’s GDP. 142 billion euros came from Eurozone’s bailout fund, 27% of it taken from German taxpayers (without their consent). The ECB lent 27 billion euros. The IMF was responsible for 32 billion euros. On his website, David Stockman argues that Greece had been on a steady path toward bankruptcy for 25 years, and since the IMF loan was made to a bankrupt, i.e., it was fraudulent conveyancing, it should be repudiated.

But the beauty of the Absolute Repudiation strategy is that it does not depend on the fraudulent conveyancing argument. No generation should have the right to bind future generations, unborn or at least not of voting age, which did not vote to be born into debt that was spent on consumption by previous generations. In fact, no single citizen has the right to bind another citizen with whom he shares a government. National debt is in the nature of an unconscionable contract created by politicians interested in their own reelection; funds so raised are often frittered away by making handouts at the cost of their hardworking citizens, and such contracts should be rescinded.

Besides the supra-nationals and some Greek banks, there is the French bank Société Générale, the German banks Commerzbank and Deutsche Bank, and French insurance groups CNP and Groupama, all of whom are owed several billion euros each. A full 48 billion euros of the 254 billion euro bailout loan went to bail out financial institutions, most of the rest was used to do a round robin repayment of existing loans. The troika (the IMF, the ECB, and the European Commission) is not interested in bailing out Greek citizens.

Historically, Greece had one of the lowest suicide rates in the world, said a Vienna University paper, arguing that austerity had increased suicide rates, which peaked in 1993 and then followed a downward trend until 2008. However, in the aftermath of the financial crisis it has increased markedly, the authors argue, more recently illustrated with a very public suicide of a 77-year- old Greek pensioner shooting himself in the head with a handgun, near the Greek Parliament building.

Historically, Greece had one of the lowest suicide rates in the world, said a Vienna University paper, arguing that austerity had increased suicide rates, which peaked in 1993 and then followed a downward trend until 2008. However, in the aftermath of the financial crisis it has increased markedly, the authors argue, more recently illustrated with a very public suicide of a 77-year- old Greek pensioner shooting himself in the head with a handgun, near the Greek Parliament building.

With his pension slashed by austerity, retired pharmacist Dimitris Christoulas left behind the following suicide note:

“The Tsolakoglou government has annihilated all traces for my survival, which was based on a very dignified pension that I alone paid for 35 years with no help from the state. And since my advanced age does not allow me a way of dynamically reacting (although if a fellow Greek were to grab a Kalashnikov, I would be right behind him), I see no other solution than this dignified end to my life, so I don’t find myself fishing through garbage cans for my sustenance. I believe that young people with no future, will one day take up arms and hang the traitors of this country at Syntagma square, just like the Italians did to Mussolini in 1945.″

The world economy is strongly interconnected, particularly in the sovereign debt market. Everyone is a lender and borrower in varying proportions. An argument against repudiation is that it would encourage others—notably Portugal, Ireland, Italy, and Spain, to emulate the Greek show of courage. The domino effect would put pressure on France, which is itself heavily indebted. But that in fact is the strongest argument in favour of repudiation. Ending the fantasy of sovereign debt will be excellent for Capitalism.

Greece, under the military junta rule, enjoyed spectacular economic growth for decades, far superior to the record of the welfare-state democracy.

How exactly will Greece recover? It will reinstitute the drachma, and the markets would initially cane the currency. Imports would become very expensive, but to start with, tourism could boom if law and order can be maintained. If the economy can be freed (not easy for a Far Left government), growth would be restored. After all, Greece, under the military junta rule, enjoyed spectacular economic growth for decades, far superior to the record of the welfare-state democracy—“After the fall of the military dictatorship even the conservative government nationalized banks and corporations, subsidized firms, and increased the powers of the welfare state.” Then the deterioration came.

Not that Greece is alone. Post-war Germany, which benefited from forgiveness of 50% of its sovereign debt, created one of the greatest economic miracles of the 20th Century, swiftly taking a war-ravaged post WWII economy to the top of Europe in just two decades, with the elimination of price controls and liberalization—this, at a time, when a large majority of its working-age men were dead. Even Spain, moving into a partially-freed market economy, achieved a 15-year economic boom under Dictator Franco.

Sure, many banks, including Greek banks, will become insolvent if repudiation happens. But insolvency is a reflection of capital structure, not of whether a business is sustainable. As long as operating revenues exceed operating costs plus an allowance for asset replacement, a business is likely to have value. If the value is less than its capital structure, then the business can get reorganized, whether in Chapter 11 (U.S.) or by private negotiation and sale. Bank shareholders and high-ranking employees would lose heavily. Wholesale creditors and perhaps even retail depositors may lose a portion of their savings. But banks would reopen for business, and perhaps not shut down at all.

Europe has done it before, as has Greece. It will not be easy, but once debt repayments and interest are eliminated, they do not need a primary budget surplus. The drunkard holds the key. Vaporize the sovereign debt, free the economy, and maintain law and order—it’s the formula that will work for all, including France and the U.S., when their turn comes. Vaporizing the debt shuts down the ability to borrow again, or even to print money—the floating-rate-exchange world is watching. No “balance-the-budget” amendment is necessary—the alcoholic throws out the bottle for good.

By delivering much of the pain to where it belongs, including catching tax-evading cronies, and eliminating industry subsidies, the drunkard can restore justice. The unidentified enemy is not the liberals fantasizing about the ECB or the State “Keynesian money-printing and devaluation (like Paul Krugman does here),” it is the cronies wanting to save their own asses.

About the Author: Vinay Kolhatkar

« University Education As It Might Be and Ought To Be: Part II I Run a Private School – and I’m Against School Vouchers »

{kind=link}