“Stakeholder Capitalism” Is a Trojan Horse for Fascism

If you wholly own a car, how would you feel if your local councilor can dictate a day a week when you must lend it to a complete stranger?

If you wholly own a car, how would you feel if your local councilor can dictate a day a week when you must lend it to a complete stranger?

If you wholly own an apartment, how would you feel if the local parish was given the right to inject two new residents to live in it, picked at their discretion, and at your cost, too?

Now consider a case where you have a “fractional ownership” of a holiday home. This means the initial outlay and costs are split among a group of owners. Typically, you may get to use it (or rent it out to your monetary benefit) one week every year, say, by scheduling your right to do so. A deed may govern the rights of usage and transfer and the obligations to contribute your “share” toward maintenance and other dues.

Shareholders in aggregate are 100% owners of corporations, but each shareholder is a fractional owner. As a group of owners, shareholders’ rights and obligations are governed by contracts they enter into explicitly (via shareholder agreements in privately-owned, unlisted corporations), or, in publicly-listed corporations, their rights are set out at law. Shares in publicly-listed entities typically come with no further obligations to make contributions, only with rights to participate in a new capital raise, vote at shareholder meetings, sell shares, etc.

The idea that third parties should have a divine right to dictate to shareholders what other interests the corporation they own (in aggregate) must serve is absurd.

The idea that third parties should have a divine right to dictate to shareholders what other interests the corporation they own (in aggregate) must serve is absurd. It’s as nonsensical as bureaucrats and priests having a right to dictate to us how we must use assets we own.

The law already contains provisions to penalize fraud and deception. Shareholders qua shareholders, and indeed, corporations as legal entities in their own right, are subject to law.

Capitalism

We think of capitalism as a political system. To use Ayn Rand’s words, the authentic version is “a full, pure, uncontrolled, unregulated laissez-faire capitalism—with a separation of state and economics, in the same way and for the same reasons as the separation of state and church.”

Every citizen and resident of a nation-state is a stakeholder (an affected party) in the social, economic, and political systems that govern that nation. Communism, capitalism, and fascism are systems that need no prefix to suggest a specific class of stakeholders redefines them.

And yet, a dangerous redefinition is what’s suggested by the term “stakeholder capitalism.”

What is Fascism?

Before we turn to how the redefinition moves individuals toward ceding control to the collective, let’s pause to assess what we mean by fascism.

To use Ayn Rand’s words again, “The main characteristic of socialism (and of communism) is public ownership of the means of production, and, therefore, the abolition of private property. The right to property is the right of use and disposal. Under fascism, men retain the semblance or pretense of private property, but the government holds total power over its use and disposal.”

It’s that kind of partial fascism that “stakeholder capitalism” moves us further toward. By design.

Now let’s ask: Who owns corporations? Who is being given the right to interfere in how the asset is to be used? It may not be “total power,” but, it’s a partial infringement of the rights of owners over their assets nevertheless.

It’s that kind of partial fascism that “stakeholder capitalism” moves us further toward. By design.

The Debate over Corporations

In the seventies, a senseless debate commenced over the question of who actually owned corporations even though the word “shareholder” says it all. In 1970, Milton Friedman asserted, in the New York Times no less (how the times have changed), that:

There is one and only one social responsibility of business—to use its resources and engage in activities designed to increase its profits so long as it stays within the rules of the game, which is to say, engages in open and free competition without deception [or] fraud.

The corporation, said Friedman, has no social responsibility:

If this statement [that the corporate executive has social responsibility] is not pure rhetoric, it must mean that he is to act in some way that is not in the interest of his employers. For example, that he is to refrain from increasing the price of the product in order to contribute to the social objective of preventing inflation, even though a price increase would be in the best interests of the corporation. Or that he is to make expenditures on reducing pollution beyond the amount that is in the best interests of the corporation or that is required by law in order to contribute to the social objective of improving the environment. Or that, at the expense of corporate profits, he is to hire ‘hardcore’ unemployed instead of better-qualified available workmen to contribute to the social objective of reducing poverty.

In each of these cases, the corporate executive would be spending someone else’s money for a general social interest. Insofar as his actions in accord with his ‘social responsibility’ reduce returns to stockholders, he is spending their money.

Friedman was misinterpreted by many as implying that executives are merely the servants of the shareholders. But he never actually said this, nor did he imply it.

In 2005, John Mackey, CEO of Whole Foods, professed disagreement with Friedman’s (valid) view that shareholders, the owners, must set the purpose for the corporations they own, without actually realizing he was in agreement with Friedman:

I’m a businessman and a free market libertarian, but I believe that the enlightened corporation should try to create value for all of its constituencies.

I believe the entrepreneurs, not the current investors in a company’s stock, have the right and responsibility to define the purpose of the company. It is the entrepreneurs who create a company, who bring all the factors of production together and coordinate it into [a] viable business. It is the entrepreneurs who set the company strategy and who negotiate the terms of trade with all of the voluntarily cooperating stakeholders–including the investors. At Whole Foods we “hired” our original investors. They didn’t hire us.

Friedman countered that Mackey’s view was equivalent to his:

The social responsibility of business to increase its profits and Mackey’s statement that ‘The enlightened corporation should try to create value for all of its constituencies’ are equivalent.

It may well be in the long run interest of a corporation that is a major employer in a small community to devote resources to providing amenities to that community or to improving its government.

T.J. Rodgers, founder and CEO of Cypress Semiconductors, was more scathing of Mackey:

Mackey spouts nonsense about how his company hired his original investors, not vice versa. If Whole Foods ever falls on persistent hard times—he will quickly find out who has hired whom, as his investors fire him.

In economic literature, Friedman’s tenet is referred to as shareholder primacy. In 2002, Professor Stephen Bainbridge offered an alternative “director primacy” view that put the Board in control. Mackey’s view could be termed as entrepreneur or management primacy. However, in each case, we have some class in ultimate control, suggestive of a master-servant relationship.

The corporation is a “nexus of contracts.”

But need there be any primacy at all?

To gauge who is right or wrong here, it’s illuminating to go back to the seventies. In 1976, professors Michael Jensen and William Meckling wrote one of the most seminal phrases in all of finance theory by revisiting the concept of the firm as a system of relationships (which was extant in academe since the thirties)—the corporation, they said, is a “nexus of contracts.”

In a free society, such contracts are entered into voluntarily by individuals, whether that be a contract between a cleaner and a cleaning company, or between an office-cleaning company and a large multinational, or between a CEO and a large corporation.

Mackey may have originally sought investors for an idea, but he is wrong to generalize the investor class as passive—private-equity investors often seek operating management severely constrained by tight contracts, while themselves setting corporate strategy. He is also wrong to assume he “hired” investors. He invited investors to contract with him, i.e., hire him as CEO to pursue a vision, including a return for investors, and some investors voluntarily agreed to do so. In the subsequent “contract,” the firm as a legal entity (the nexus) hired Mackey as CEO, and that set forth the future relationship, even if Mackey initiated the invitation.

To illustrate, if I agree to buy your used car, it matters not who made the first approach once a contract is executed—the contract sets out our rights and obligations going forward.

Thus, corporations are legal entities that act as a nexus of voluntary contracting among informed individuals. The ownership and control debate should have ended there.

To quote Ayn Rand once again:

In a capitalist society, all human relationships are voluntary. Men are free to cooperate or not, to deal with one another or not, as their own individual judgments, convictions, and interests dictate. They can deal with one another only in terms of and by means of reason, i.e., by means of discussion, persuasion, and contractual agreement, by voluntary choice to mutual benefit. The right to agree with others is not a problem in any society; it is the right to disagree that is crucial. It is the institution of private property that protects and implements the right to disagree—and thus keeps the road open to man’s most valuable attribute (valuable personally, socially, and objectively): the creative mind.

There is no other form of capitalism.

Stakeholder Capitalism

And yet, we have “stakeholder capitalism,” defined by Investopedia as:

Stakeholder capitalism is a system in which corporations are oriented to serve the interests of all their stakeholders. Among the key stakeholders are customers, suppliers, employees, shareholders, and local communities.

In this version of “capitalism,” the property owners/shareholders, it seems, are no more significant than local communities and suppliers.

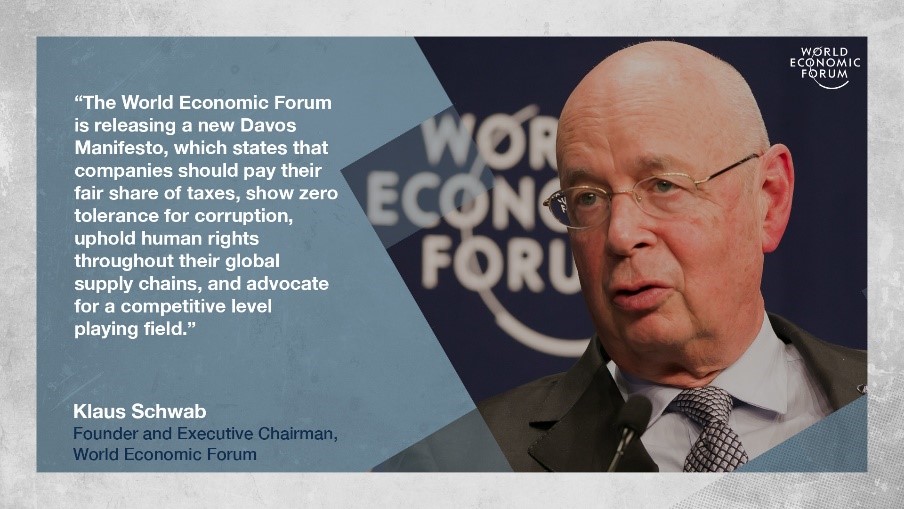

Professor Klaus Schwab, founder and Executive Chairman, World Economic Forum (WEF), made “stakeholder capitalism” the theme of Davos 2020, pompously titling his essay: “Davos Manifesto 2020: The Universal Purpose of a Company in the Fourth Industrial Revolution.”

Professor Klaus Schwab, founder and Executive Chairman, World Economic Forum (WEF), made “stakeholder capitalism” the theme of Davos 2020, pompously titling his essay: “Davos Manifesto 2020: The Universal Purpose of a Company in the Fourth Industrial Revolution.”

Thanks, Professor Schwab. What we shareholders may own has a “universal” purpose determined by limousine liberals at five-star facilities in fancy resorts. Davos, by the way, is a picturesque, alpine getaway, one of Switzerland’s biggest ski resorts. It plays host to WEF’s annual meeting of global political and business elites at the end of January. That annual meeting is now often referred to simply as “Davos.”

At Davos 2020, said WEF on their website, “We will aim to give concrete meaning to “stakeholder capitalism,” assist governments and international institutions in tracking progress towards the Paris Agreement …”

Also, on the WEF website, Alex Edmans, a professor of finance at London Business School says:

Today it’s [Friedman’s article] an object of scorn and ridicule. It’s been cited over 20,000 times, yet most of these citations are to highlight how broken shareholder capitalism is. 3,000 of those citations have come in the past year, as the stakeholder capitalism movement has gathered momentum. To declare that you reject the Friedman doctrine has become almost a requirement for acceptance into polite society.

There are several problems with Edmans’ essay. Chief among them is contrasting “stakeholder” capitalism with “shareholder” capitalism, as though there were two authentic variants of capitalism. Which there are not, whether in corporate finance theory or political philosophy.

But right there, at the end of the quote, comes the “neo-Marxist” admission, worth reiterating:

To declare that you reject the Friedman doctrine has become almost a requirement for acceptance into polite society.

Like buying into climate alarmism, Black Lives Matter, and other neo-Marxist narratives.

However, to his credit, Edmans concedes that:

Friedman never advocated that companies exploit stakeholders. He argued that it is legitimate for a company to focus on increasing profits because the only way it can do so, at least in the long term, is if it treats stakeholders seriously.

While last year’s Business Roundtable statement was heralded as ‘The end of Friedmanism,’ it’s fully consistent with it. Any company maximizing shareholder value needs to commit to delivering value to customers … investing in employees … dealing fairly and ethically with suppliers … [and] supporting the communities in which [they] work.

I see. The elites of the “Business Roundtable” believe that shareholders could be well served by delivering shoddy products to customers or by dealing unethically with suppliers.

Edmans makes another concession:

Indeed, critics of shareholder value attack it for being short-termist, but this makes no sense because shareholder value is an inherently long-term concept. Shareholder value is the present value of all future cash flows that a company generates. That’s not just abstract theory—it holds in practice.

Shareholder “value” is a valid concept. And, in this quote, Edmans is dead right on finance theory and practice.

Delusion or Design?

That shareholders cannot be well served by a corporation that treats its customers or employees unfairly is obvious. One may dismiss the distinction of two types of capitalism as simply a benign delusion. But Davos has always been an instrument of neo-Marxist social engineering, an evil by design.

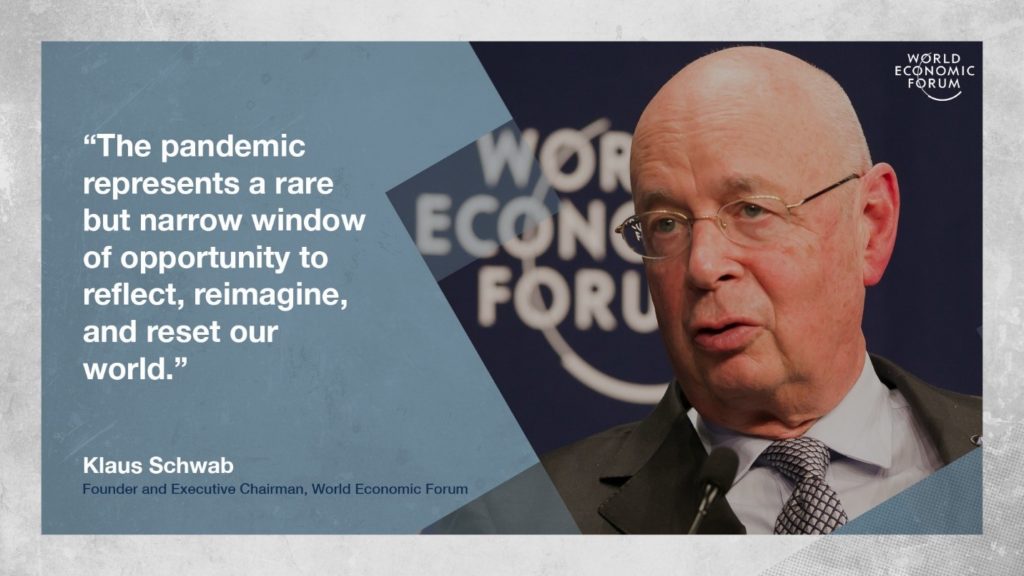

Consider, for instance, the agenda of Davos 2021. The theme is “The Great Reset.” (The meeting has been postponed to May 2021 and moved to Singapore).

Schwab, unabashedly calling the pandemic “a rare opportunity,” says The Great Reset will “offer insights to help inform all those determining the future state of global relations, the direction of national economies, the priorities of societies, the nature of business models and the management of a global commons.”

Schwab, unabashedly calling the pandemic “a rare opportunity,” says The Great Reset will “offer insights to help inform all those determining the future state of global relations, the direction of national economies, the priorities of societies, the nature of business models and the management of a global commons.”

Having driven a stake through true capitalism by redefining corporations, Schwab now foresees that “the Great Reset will require us [note the collective “us” pulled into their vision] to integrate all stakeholders [emphasis mine] of global society into a community of common interest, purpose, and action.” With the foundation laid in 2020, Schwab sets out his ambitious goal:

We need a change of mindset, moving from short-term to long-term thinking, moving from shareholder capitalism to stakeholder responsibility. Environmental, social and good governance have to be a measured part of corporate and governmental accountability.

In other words, since trillion-dollar corporations belong to the collective “us,” the “stakeholders,” we can now use their resources to achieve “our” neo-Marxist goals of equalizing outcomes (not opportunities), using divisive chants of racism, sexism, and environmental injustice (which will veer even more control and power toward the wannabe masters who cloak themselves as “public servants”—but serve us, they don’t).

“Other influential leaders echoed Mr. Schwab’s call.” Naturally. Member states of the United Nations, too, have enthusiastically signed onto The Great Reset.

From July 2020, Schwab began to admonish us: If we don’t use the COVID-19 pandemic as a “timely opportunity” to reset the world, the next big thing could be a cyber pandemic that would halt power supplies, transportation, hospitals etc.—“COVID-19 would be a small disturbance in comparison to a major cyber attack”—he says it like it’s a forewarning.

Is Schwab truly concerned that over a hundred million privately-owned servers worldwide will be infected simultaneously, or is he a purveyor of panic? If, like me, you are inclined to believe that the WEF Chairman is a purveyor of panic, ask yourself what his agenda is.

Will the Republicans Save Us?

And don’t expect the Republicans to show clarity of thought. Their zeal is outdone only by extent of their ignorance. Steve Denning reported in Forbes:

Since 2015, Democratic senators, including Minority Leader Chuck Schumer and Senator Tammy Baldwin, have been pushing the Securities & Exchange Commission to do something about MSV [maximizing shareholder value].

In 2019, Republicans joined in. In May 2019, the Republican-led Senate Committee on Small Business and Entrepreneurship, faulted CEOs for focusing too much on the next quarter and not enough on the next generation: ‘Many business leaders,’ said the committee chair, Senator Marco Rubio, ‘seem to care more about returns for shareholders than the people who work for them.’

Thanks, Mr. Rubio. We were not aware that you are a mind-reader as well.

At least Nikki Haley, former ambassador to the U.N., retained some clarity:

Some conservatives have turned against the market system. They tell us America needs a … different kind of capitalism. A hyphenated capitalism. [Senator Rubio calls his version “common good capitalism”]. Yet while these critics keep the word capitalism, they lose its meaning. They want to give government more power to make more decisions for businesses and workers. They differ from the socialists only in degree.

Hyphenated capitalism is no capitalism at all. The better name for it is socialism lite.

Bang on target, Ms. Haley.

About the Author: Vinay Kolhatkar

« Vaccine Ethics: If You Are Not “Essential,” Just Wait—or Die Which of These Is 2020’s Greatest “Crime against Humanity”? »