Translating deep thinking into common sense

Does Fractional Reserve Banking Cause Inflation?

By Dale B. Halling

January 7, 2017

SUBSCRIBE TO SAVVY STREET (It's Free)

This article is a continuation of the article “What is Money?”

A fractional reserve bank is doing something analogous to what engineers have done with the telephone system. The backbone that connects two people together on a phone line does not have the capacity to allow everyone to make a call at the same time.

The first ‘banks’ in Europe after the Dark Ages were goldsmiths. Because goldsmiths were working with valuable materials they needed vaults. Wealthy patrons would often give some of their gold or other valuables to the goldsmith to secure in their vault. The goldsmith would give the patron a receipt for their gold. Over time, just like the clay tablets for grain, people started to trade the receipts instead of taking out gold and paying with the gold.

Some of the customers also started asking for loans. The goldsmiths wanted to reduce their risk if the customer defaulted on the loan, so they asked for collateral. Originally, they probably asked for jewelry or other things made of silver and gold, since they knew they could liquidate (sell) these items fairly easily. The goldsmiths could have given the customer gold out of their gold reserve (capital) and they probably did initially. Most likely many customers then gave the gold back to the goldsmith and took receipts for the gold. If the goldsmith’s receipts were trusted enough, they could skip this step and just give the customer receipts as collateral. If the customer failed to pay the loan back, the jewelry (collateral) became the property of the goldsmith.

Or the goldsmiths could have given the borrower gold on deposit from other customers, which is the way most people think of banking working. In that case then the gold the goldsmith had on hand (deposit) was less than the amount of the receipts outstanding for the gold, which is fractional reserve banking (assuming the goldsmith had no gold capital or the loan(s) were greater than the goldsmith’s gold capital). Fractional reserve banking is defined as:

A banking system in which only a fraction of bank deposits are backed by actual cash on hand and are available for withdrawal.[1]

Most customers probably deposited the borrowed gold with the goldsmith and took receipts. Again the goldsmiths probably began to skip the step of giving the borrower actual gold (silver) and just gave them receipts for the gold. At this point it might appear that the goldsmith is “creating money out of thin air,” however the receipts in this case are backed by the collateral, jewelry in this example. Actually, all the outstanding receipts are now backed by the gold on hand and the collateral the goldsmith has for loans.

At this point the goldsmith risks all the holders of these receipts asking for their gold and the goldsmith does not have enough gold to fulfill all these demands. However, the goldsmith does have enough capital to fulfill actual demand, because the collateral, jewelry and gold on deposit in this example, is enough to meet the demand. It is likely that initially most of these loans were “callable,” meaning that the goldsmith could demand the borrower pay them back in full (gold or receipts) at any time. If the borrower paid up, then the goldsmith had no problem paying off the receipts. If the borrower did not pay up, then goldsmith became the owner of the collateral (jewelry) and could sell it to fully back the receipts.[2]

Eventually the goldsmiths realized it was not only jewelry (gold and silver items) that had value and could act as collateral. For instance, arable farmland was one of the most valuable assets that people could own for most of history since the Agricultural Revolution. The goldsmith could not put the farmland in his vault, however he could have a document evidencing a legal claim to the land. That claim stated that if the borrower did not pay back the loan, then the goldsmith became the owner of the farmland. Of course it takes longer to liquidate farmland than jewelry, and farmland might be more subject to market value fluctuations. As a result, the amount the goldsmith would lend against the farmland was lower than for gold and silver items.

At first goldsmiths probably made loans against farmland that someone owned outright. Eventually, they figured out that they could make loans on farmland that was being purchased, as long as there was a big enough down payment (the equivalent of loaning less than the value of collateral). What the goldsmith is doing is securitizing assets other than gold. When the goldsmiths created receipts for gold and silver deposits they were securitizing gold (and silver). “Securitization is a pooled group of financial assets that together create a new security”[3] or banknote in this case. This means that goldsmith receipts (banknotes) are backed by not only gold deposits but the other assets that they hold as collateral.

This is exactly what a company does when it sells bonds (stock). The bond is backed by the assets (collateral) of the company. The bonds are usually very liquid and can be sold or traded in exchange for goods and services, i.e., the bonds are money.

These goldsmiths became fractional reserve banks once they started securitizing assets other than gold. Fractional reserve banking is an important invention and is created (exists) in a free market. A fractional reserve bank is doing something analogous to what engineers have done with the telephone system. The backbone that connects two people together on a phone line does not have the capacity to allow everyone to make a call at the same time. The engineers know that only a certain fraction of people will normally be on their phones at the same time. By designing a system to handle this level of usage plus a margin, the cost of the telephone system is reduced. Of course occasionally, like in the time of an emergency, everyone wants to use their phone at the same time and then you receive a message like ‘all circuits are busy, please try your call again later.’ Another example is the time sharing of resources is done by computers. Before the 1980s this was done by having a number of computer terminals all connected to one large computer that time shared its resource among these terminals. This is still done within your computer when it runs multiple programs. The processing power of the microcontroller is time shared among these programs.

Banks know that only a small number of people will want gold at the same time. Most of the time people will be happy with banknotes or just accounting entries. However, if people lose confidence in the bank, then they will all want to withdraw gold (cash) at the same time. This is called a ‘run on the bank’ and is similar to everyone trying to make a telephone call at the same time. Note that this is a cash flow issue and can happen even to a bank that is profitable. Usually, banks that were clearly profitable could borrow gold from other banks to weather the run.

When a fractional reserve bank (hereinafter bank) initiates a loan against an asset, let’s say a farm, the bank creates a security (banknotes or an entry in a ledger) equal to the amount of the loan. In this process it “creates money” equal to the loan. At one time this might have been done by printing a bunch of banknotes, but now it is an electronic entry in the banks accounting system. An article entitled “Money Creation in the Modern Economy” published by the Bank of England explains “whenever a bank makes a loan, it simultaneously creates a matching deposit in the borrower’s bank account, thereby creating new money.”[4] This article also points out that “money creation in practice differs from some popular misconceptions — banks do not act simply as intermediaries, lending out deposits that savers place with them, and nor do they ‘multiply up’ central bank money to create new loans and deposits.”[5] According to the article, “Money in the Modern Economy: an Introduction”, there are three main sources of money in modern economies, currency, bank deposits (loans by commercial banks) and central bank reserves.[6] This article also points out that most money in the economy is created by banks initiating loans. [7]

Some people call this debt money and argue it is bad for the economy.[8] They imply that this system of money creation requires we pay interest to have money. First, it is important to point out that this sort of money creation happens in a free market. Second, the only one paying interest is the person who took out the loan. In a free market there would also be other forms of money, such as gold, silver, bitcoin etc.

When loans are paid back the money is removed from the economy, just like the case of the clay tablets being destroyed (taken out of circulation) when people turned them in for their grain. The bank no longer has access to the collateral (e.g., farmland, jewelry, etc.). As a result, the banknotes (electronic entries) are no more. Note that money is also removed if the borrower defaults on the loan.

In a free market (for this discussion most importantly means no legal tender laws and no central bank) banks’ ability to ‘create money’ is limited by the value of the assets used as collateral.[9] The bank is not creating money, it is securitizing assets and the banks’ ability to create money is then limited to the assets that can be securitized.

If the banks create too many loans that cannot be paid back, then they will tighten their lending standards. This will result in fewer loans and less money being created. When the economy is growing banks will fund more loans and create more money. However, the amount of money in the economy will be proportional to the assets that can be collateralized in the economy.

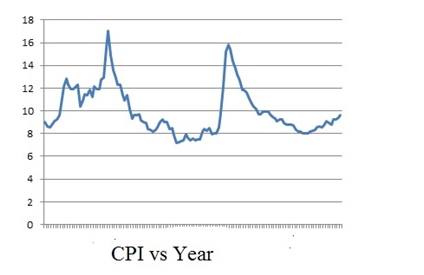

As a result, in a free market fractional reserve banks do cause variations in the money supply, but do not cause inflation or deflation. Note that the United States had fractional reserve banks from before the Revolution and yet the United States did not have any periods of inflation. This chart shows the consumer price index (CPI) from 1787 to 1913, with the base year of 1982-84 being equal to 100. 1787 is the year the U.S. Constitution was ratified and 1913 is the year the Federal Reserve (central bank) was created. The United States had fractional reserve banks throughout this time period. Note that the CPI is essentially the same over this period which means there was no net inflation and also this chart does not differentiate between changes in supply and inflation.[10]

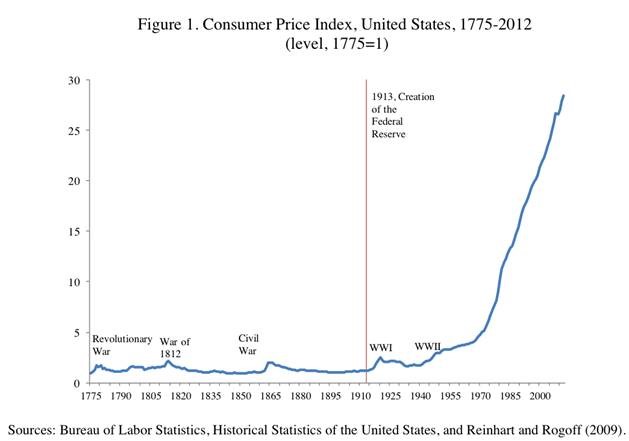

Here is another chart on point that shows inflation did not occur until the United States started a central bank (The Federal Reserve), despite fractional reserve banks existing before the Fed.[11]

Inflation did not occur until the United States started a central bank (The Federal Reserve), despite fractional reserve banks existing before the Fed.

Banks were constrained in how much money they could create. Now prices did vary widely sometimes, particularly in times of war. However it is necessary to separate out the fluctuation in prices due to changes in supply and demand from those due to changes in the quantity of money. During a war (crop failure) there is an increase in the demand for goods and services, particularly food. Men are away fighting a war instead of planting their fields and the war itself often destroys the crops on large tracks of land. This increase in the price of food will mean that farmland that is not threatened by the war will be more valuable. As a result, it is likely banks will be willing to lend more money against these farms. This will result in some increase in the money supply. However, when the war ends the prices of the farm goods will fall and so will the value of the farmland, which will reduce the number of loans outstanding, reducing the amount of money in the economy. Averaged out over time, money grows at the same rate as the economy and prices are roughly stable.[12]

This is what we have learned about banking in a free market:

1) Fractional reserve banking can exist in and is an invention of a free market.

2) Fractional reserve banks do create and destroy money, however the amount of money created is proportional to the assets in an economy.

3) Fractional reserve banks do not cause inflation.

________________________________________________________________________________________________________________________________________________________________________________________________

[1] Fractional Reserve Banking Definition | Investopedia http://www.investopedia.com/terms/f/fractionalreservebanking.asp#ixzz4QUDQvzpR, accessed November 19, 2016.

[2] The collateral is usually worth more than the loan to deal with market fluctuations. This is why people used to say that a bank would only loan you money if you were already rich.

[3] Securitize Definition | Investopedia http://www.investopedia.com/terms/s/securitize.asp#ixzz4QVLtJy4H, accessed on November 19, 2016.

[4] Michael McLeay, Amar Radia and Ryland Thomas, Money creation in the modern Economy, http://www.bankofengland.co.uk/publications/Documents/quarterlybulletin/2014/qb14q102.pdf, accessed November 19, 2016.

[5] Michael McLeay, Amar Radia and Ryland Thomas, Money creation in the modern Economy, http://www.bankofengland.co.uk/publications/Documents/quarterlybulletin/2014/qb14q102.pdf, accessed November 19, 2016.

[6] Michael McLeay, Amar Radia and Ryland Thomas, Money in the modern economy: an introduction, http://www.bankofengland.co.uk/publications/Documents/quarterlybulletin/2014/qb14q101.pdf, accessed November 19, 2016.

[7] Michael McLeay, Amar Radia and Ryland Thomas, Money in the modern economy: an introduction, http://www.bankofengland.co.uk/publications/Documents/quarterlybulletin/2014/qb14q101.pdf, accessed November 19, 2016.

[8] Debt-Based Money vs. Sovereign Money, http://positivemoney.org/our-proposals/debt-based-money-vs-sovereign-money-infographic/, accessed November 19, 2016.

[9] Credit cards and personal loans may seem to violate this, but a person’s willingness to work is an asset.

[10] Measuring Worth, https://www.measuringworth.com/uscpi/result.php, accessed January 4, 2017.

[11] Shifting Mandates: The Federal Reserve’s First Centennial, Carmen M. Reinhart and Kenneth S. Rogoff, For presentation at the American Economic Association Meetings, San Diego, January 5, 2013

[12] JOSH ZUMBRUN, A Brief History of U.S. Inflation Since 1775, http://blogs.wsj.com/economics/2015/12/14/a-brief-history-of-u-s-inflation-since-1775/, accessed 12/3/2016.

-

Affirmative Action for Intellectual Diversity?

-

“Deep Learning”—But Is It Conscious?

-

AI: Intimations of “Emergence”

-

The Neuroscience of Cringe: Why the Past Still Burns

-

The 2025 Election: Australia vs the Global Deep State

-

Why the Trump-Musk Tour of Fort Knox Matters

-

A Meeting of Minds

-

Abortion and the Minimum Wage Law

-

Federalism or Anti-Federalism—That is the Question

-

A Most Humane Solution for All Peace-Loving Gazans